When Should a Startup Get a 409A Valuation?

A practical guide to the timing, triggers, and compliance deadlines that determine when your startup needs an independent 409A valuation — and what happens if you wait too long.

Key Takeaways

- check_circleEvery startup must obtain a 409A valuation before issuing stock options or any deferred compensation to employees.

- check_circleA new 409A valuation is required at least every 12 months or after any material event — whichever comes first.

- check_circleMaterial events that trigger a new valuation include fundraising rounds, significant revenue changes, M&A activity, and major pivots.

- check_circleUsing an independent appraiser creates IRS safe harbor protection, shifting the burden of proof to the IRS in any dispute.

- check_circleFailing to comply with 409A can result in a 20% penalty tax plus interest on affected employees — not the company.

Introduction

One of the most common questions early-stage founders ask is: "When do we actually need a 409A valuation?" The short answer is simple — before you grant your first stock option. But the full picture involves understanding IRS timing rules, material events, safe harbor protection, and the very real penalties for getting it wrong.

This guide walks through every scenario where a 409A valuation is required, when to refresh an existing one, and how to stay compliant as your company grows — whether you're a founder managing equity yourself or a CPA firm advising startup clients.

What Is a 409A Valuation?

A 409A valuation is an independent assessment of your company's fair market value (FMV) of its common stock. It's required under IRC Section 409A to set the exercise price for stock options and other forms of deferred compensation. The valuation must be performed by a qualified, independent appraiser to receive safe harbor protection.

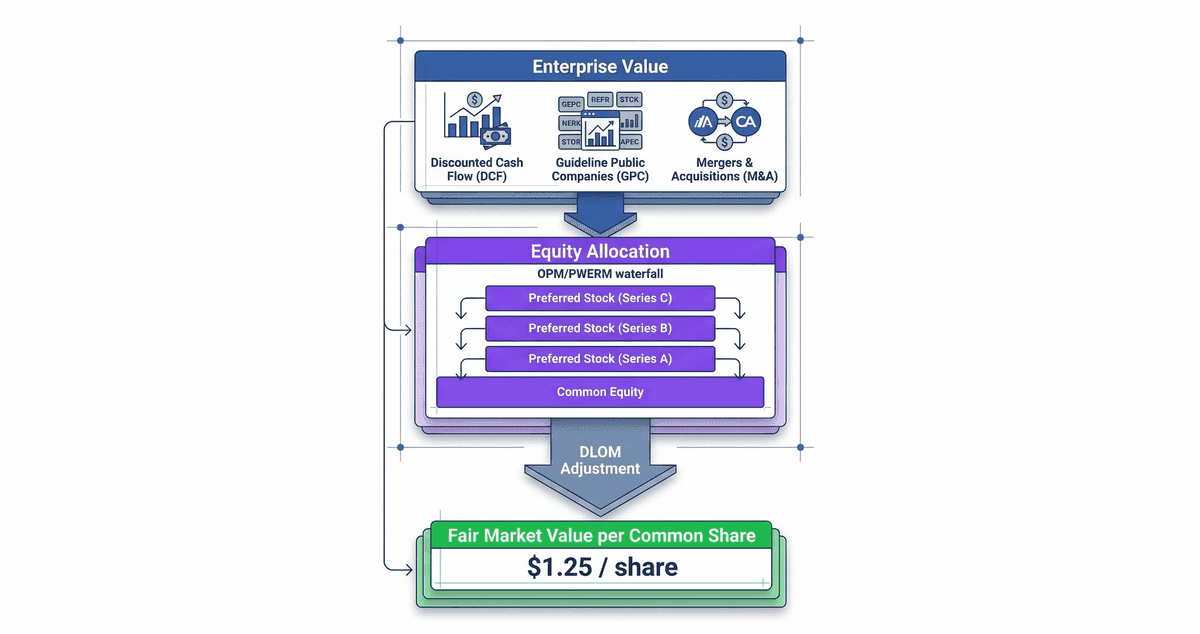

A proper 409A valuation isn't just a number — it's a comprehensive report that documents the methodology, assumptions, and market data used to arrive at the FMV conclusion. This documentation is critical when auditors or the IRS review your option pricing. Valuation methodologies typically include income approaches like Discounted Cash Flow (DCF), market approaches using Guideline Public Company (GPC) multiples, and equity allocation methods such as the Option Pricing Model (OPM) or Probability-Weighted Expected Return Method (PWERM).

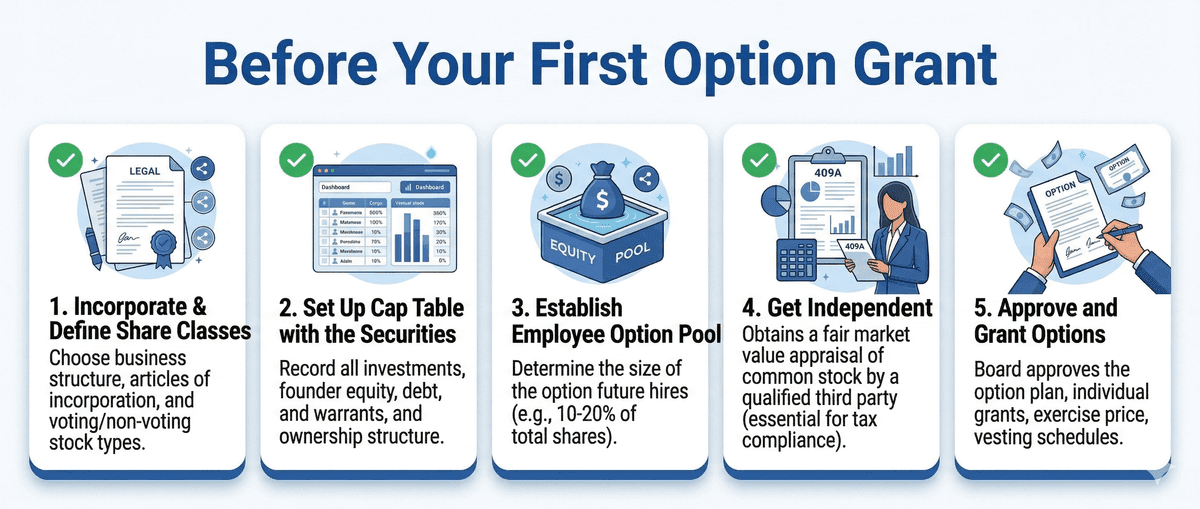

Trigger 1: Before Your First Option Grant

The most critical timing requirement is straightforward: you need a 409A valuation before granting any stock options. This applies whether you're granting to employees, advisors, or contractors. The valuation establishes the FMV that becomes the exercise price (strike price) of the options.

Many startups create an equity incentive plan early but delay getting a valuation until they're ready to make actual grants. That's perfectly fine — the valuation is tied to the grant date, not the plan creation date. However, having your cap table structured and up to date before starting the valuation process will significantly speed up delivery. A clean cap table with clearly defined share classes, option pools, and security terms is the foundation of an accurate 409A.

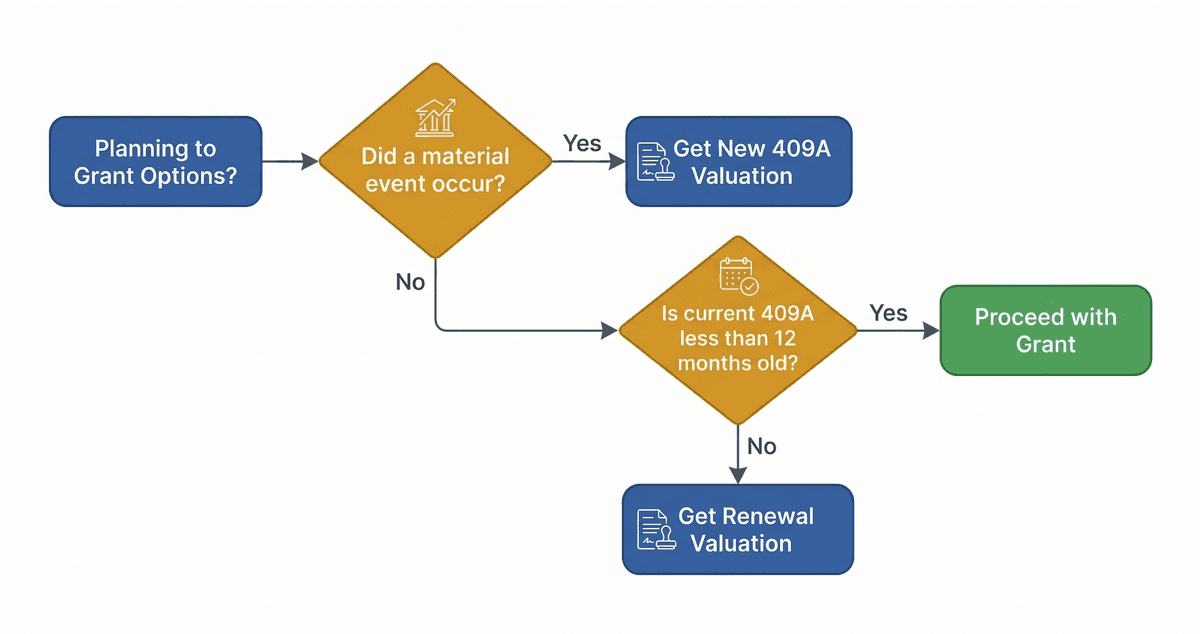

Trigger 2: The 12-Month Expiration Rule

Once you have a 409A valuation, it remains valid for a maximum of 12 months — assuming no material event occurs during that period. After 12 months, you must obtain a new valuation before granting additional options.

- Valuation dated January 15, 2026 → Valid for grants through January 14, 2027

- Any grants after January 14, 2027 require a new valuation

- Best practice: start the renewal process 2-3 weeks before expiration to avoid gaps

Trigger 3: Material Events

Even if your valuation is less than 12 months old, a material event that significantly affects the company's value will invalidate it. The IRS doesn't provide an exhaustive list, but the following events are widely recognized as triggers:

| Material Event | Why It Triggers a New 409A | Timing |

|---|---|---|

| Closing a priced equity round | Directly reprices the company's equity | Before next option grant after close |

| Signing a term sheet (near-certain close) | Signals imminent value change | Before grants after signing |

| Significant revenue milestone | Fundamentally changes financial projections | Within 30-60 days of milestone |

| Major customer win or loss | Materially impacts future cash flows | Before next option grant |

| Pivot or business model change | Changes the basis of valuation assumptions | Before next option grant |

| Key executive hire or departure | Affects company trajectory and risk profile | Before next option grant |

| M&A discussions or LOI | Creates near-term exit expectation | Immediately upon LOI execution |

| Down round or bridge financing | Signals distress or value decline | Before next option grant after close |

The 409A Timeline for a Typical Startup

Here's how the 409A valuation cycle typically plays out as a startup grows from incorporation to later-stage funding:

| Stage | Valuation Trigger | Common FMV Range |

|---|---|---|

| Incorporation | No valuation needed yet (no options granted) | N/A |

| Pre-seed / ESOP setup | First option grants to founding team | Very low (often $0.01–$0.10/share) |

| Seed round close | Priced round → material event | Typically 20–35% of preferred price |

| 12-month renewal | Annual expiration | Depends on traction |

| Series A close | Priced round → material event | Typically 25–40% of Series A price |

| Subsequent rounds | Each round is a new material event | Discount narrows as company matures |

As your capital structure grows more complex — with multiple preferred share classes, participation rights, liquidation preferences, and anti-dilution provisions — the valuation methodology must evolve to match. Early-stage companies with simple structures often use a Current Value Method (CVM) or basic backsolve, while later-stage companies with complex waterfalls require an Option Pricing Model (OPM) that uses Black-Scholes breakpoint analysis to allocate enterprise value across each security class.

What's Inside a 409A Valuation Report?

Understanding what goes into a 409A report helps you appreciate why proper methodology and documentation matter. A compliant 409A valuation typically includes:

- Company overview and cap table analysis — documenting every share class, option pool, warrant, SAFE, and convertible note

- Enterprise value determination using one or more approaches (DCF, GPC multiples, M&A comparables, or backsolve from recent financing)

- Equity allocation using OPM, PWERM, or hybrid methods — modeling the waterfall from liquidation preferences through participation rights

- DLOM (Discount for Lack of Marketability) calculation using established frameworks like Finnerty or restricted stock studies

- Fair market value conclusion with safe harbor statement and valuation certification

- Supporting appendices with comparable company data, financial projections, and assumption documentation

Safe Harbor Protection: Why It Matters

The IRS recognizes three methods that create a presumption of reasonableness (safe harbor) for your valuation. If your valuation qualifies for safe harbor, the IRS must prove it's grossly unreasonable to challenge it — a very high bar.

- Independent appraisal by a qualified individual or firm (most common for startups)

- Binding formula used consistently for all equity transactions (rarely practical)

- Board determination for illiquid startups less than 10 years old, with a reasonable application of a reasonable valuation method by someone with significant relevant experience (risky without documentation)

For most startups, Option 1 — an independent appraisal — is the gold standard. It provides the strongest protection and is what auditors and investors expect to see during due diligence. The key is ensuring the appraiser uses defensible methodologies — properly documented DCF assumptions, justified comparable company selection, and appropriate allocation models for your specific capital structure.

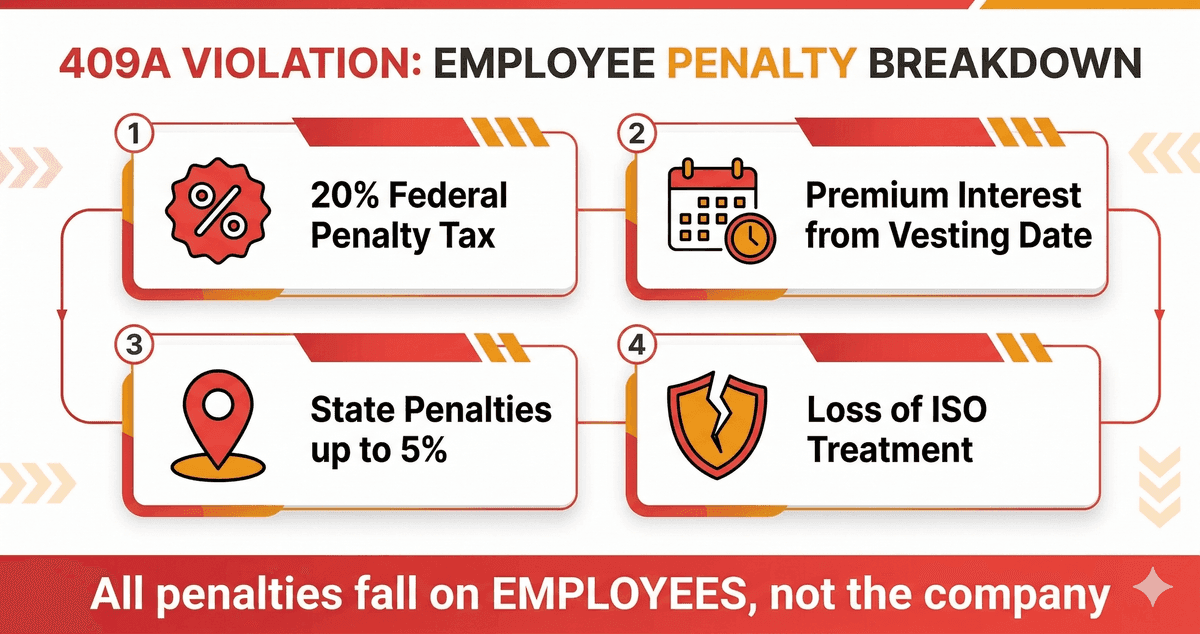

Penalties for Non-Compliance

The penalties for 409A violations are severe and fall on employees, not the company — which creates a particularly painful dynamic:

- 20% additional tax on the amount of deferred compensation

- Interest penalty calculated from the date the options first vested (not when exercised)

- Ordinary income tax on the spread at vesting (rather than the favorable treatment of ISOs)

- State-level penalties in some jurisdictions (California adds an additional 5%)

The irony of 409A penalties is that employees bear the tax consequences of a compliance failure that was entirely within the company's control. This is why investors and sophisticated hires specifically ask to see a current 409A valuation during due diligence.

Beyond IRS penalties, non-compliance creates serious downstream problems: it can delay or derail fundraising (investors will flag it in due diligence), complicate M&A transactions, and erode trust with employees who discover their options were mispriced. The cost of a proper 409A valuation is trivial compared to these risks.

How Long Does a 409A Valuation Take?

Timeline varies by provider and company complexity. Traditional firms often take 3-4 weeks, while platform-driven providers can deliver significantly faster by automating the analytical workflow. Here are typical benchmarks:

| Phase | Traditional Firm | Platform-Driven (e.g., Zimbs Valetex) |

|---|---|---|

| Data collection | 3–5 days | 1–2 hours (structured intake) |

| Cap table analysis | 2–3 days | Automated from platform data |

| Comparable company analysis | 3–5 days | 6–8 hours (GPC & M&A data integration) |

| Valuation modeling & allocation | 5–7 days | 6–8 hours (OPM/PWERM engine) |

| Draft report delivery | 3 Week | 24 Hours |

| Revisions & finalization | 3–5 days | 6-8 hours |

| Total turnaround | 3–4 weeks | 48 Hours |

Choosing a 409A Valuation Provider

Not all 409A providers are equal. When evaluating options, consider these factors:

| Factor | What to Look For | Red Flag |

|---|---|---|

| Methodology | Multiple approaches (DCF, GPC, OPM, PWERM) | Single-method "black box" valuations |

| Audit defensibility | Full documentation with assumption justification | Summary-only reports without methodology detail |

| Cap table integration | Handles complex structures (preferred, SAFEs, convertibles) | Requires manual simplification of your cap table |

| Turnaround | 7-10 days standard, rush options available | 4+ weeks with no expedited option |

| Pricing | Transparent, tiered by complexity | Hidden fees or per-revision charges |

| Support | Audit support calls, board presentation assistance | No post-delivery support |

The best providers combine platform-driven efficiency with human expert review. Fully automated online valuations may be fast and cheap, but they often lack the methodology depth needed to withstand Big 4 audit scrutiny. Conversely, traditional firms deliver thorough reports but at premium prices and slower timelines. The ideal solution sits in the middle — professional quality at startup-friendly prices with structured methodology, audit-ready documentation, and responsive turnaround.

Preparing for Your 409A Valuation

Having the right data ready before engaging a valuation provider will accelerate the process and improve the accuracy of your report. Here's what you'll need:

- Fully updated cap table with all share classes, option pools, warrants, SAFEs, and convertible notes

- Articles of incorporation and any amendments (for liquidation preferences, participation rights, anti-dilution terms)

- Most recent financial statements (balance sheet, income statement, cash flow)

- Financial projections for 3-5 years (if available — required for DCF analysis)

- Details of any recent funding rounds, secondary transactions, or term sheets

- Prior 409A valuation reports (if this is a renewal)

Conclusion

The timing of your 409A valuation isn't something to leave to chance. Get your first valuation before granting any options, refresh it every 12 months, and obtain a new one after any material event. An independent appraisal provides the strongest safe harbor protection and is increasingly expected by investors, auditors, and employees alike.

The cost of a proper valuation — whether you choose a platform-driven solution or a traditional advisory firm — is trivial compared to the 20% penalty tax, potential fundraising complications, and reputational damage of non-compliance. With modern valuation platforms offering audit-defensible reports in as little as 7-10 days, there's no reason to delay or cut corners on this critical compliance requirement.

Frequently Asked Questions

When does a startup need its first 409A valuation?expand_more

A startup needs its first 409A valuation before granting any stock options or equity-based deferred compensation. This typically happens when the company creates its first employee stock option plan (ESOP) and is ready to make initial grants. There is no minimum company age or revenue threshold — the trigger is the intent to issue options.

How often do you need to update a 409A valuation?expand_more

A 409A valuation must be updated at least every 12 months to maintain safe harbor protection. However, a new valuation is also required whenever a material event occurs — such as closing a new funding round, a significant change in revenue or business model, or any event that would meaningfully impact the company's fair market value.

What happens if a startup doesn't get a 409A valuation?expand_more

If stock options are granted without a compliant 409A valuation, the IRS can determine that the exercise price was set below fair market value. Affected employees face a 20% additional tax on the deferred compensation, plus an interest penalty that accrues from the date the options vested. The penalties fall on the employees, not the company, which creates significant liability and trust issues.

What is 409A safe harbor and why does it matter?expand_more

Safe harbor is a legal protection under IRC Section 409A that presumes your valuation is reasonable unless the IRS can prove otherwise. The most common way to establish safe harbor is by obtaining an independent appraisal from a qualified third party. Without safe harbor, the burden of proof falls on the company to demonstrate its option pricing was at fair market value.

Does a startup need a new 409A valuation after every funding round?expand_more

Yes. A new funding round is considered a material event that changes the company's fair market value. You should obtain an updated 409A valuation after closing a priced equity round before granting any new stock options. Grants issued using a pre-funding valuation after a round closes will not have safe harbor protection.

How much does a 409A valuation cost?expand_more

409A valuation costs vary widely. Traditional Big 4 firms charge $5,000 or more, while modern platforms like Zimbs Valetex offer audit-defensible valuations starting at $499 for pre-revenue startups. The cost depends on company complexity, capital structure, and turnaround time requirements.