ASC 820 Valuation: A Complete Guide to Fair Value Measurement

ASC 820 provides a clear framework for fair value measurement under U.S. GAAP. Learn about the fair value hierarchy, valuation approaches, and why compliance matters.

Key Takeaways

- check_circleASC 820 provides a unified framework for measuring fair value of assets and liabilities under U.S. GAAP.

- check_circleThe three-level fair value hierarchy classifies inputs from most reliable (Level 1: quoted prices) to most assumption-based (Level 3: unobservable inputs).

- check_circleCompanies need ASC 820 valuation for financial reporting, purchase price allocation, impairment testing, and fund valuation.

- check_circleThree valuation approaches — Market, Income, and Cost — are used depending on asset type and data availability.

- check_circleModern valuation platforms automate ASC 820 calculations, support multiple approaches, and generate audit-ready reports.

Introduction

For companies dealing with financial instruments, investments, or complex assets, accurate fair value measurement is essential. ASC 820 (Accounting Standards Codification 820) is a U.S. GAAP standard that provides a clear framework to measure the fair value of assets and liabilities for financial reporting purposes. It ensures that valuations are accurate, consistent, and transparent — helping companies maintain compliance and credibility with investors and regulators.

Understanding ASC 820

ASC 820 defines how companies should determine the fair value of their assets and liabilities. Fair value refers to the price at which an asset can be sold or a liability can be transferred in a normal transaction between market participants on a specific date. The standard provides a unified approach to fair value measurement, removing ambiguity and ensuring consistency across financial reporting.

Key Objectives of ASC 820

The main objectives of ASC 820 are centered around bringing clarity and reliability to fair value reporting:

- Standardize fair value measurement across organizations

- Improve consistency in financial reporting

- Provide transparency to investors and stakeholders

These objectives ensure that companies follow a uniform approach when reporting the value of their assets and liabilities.

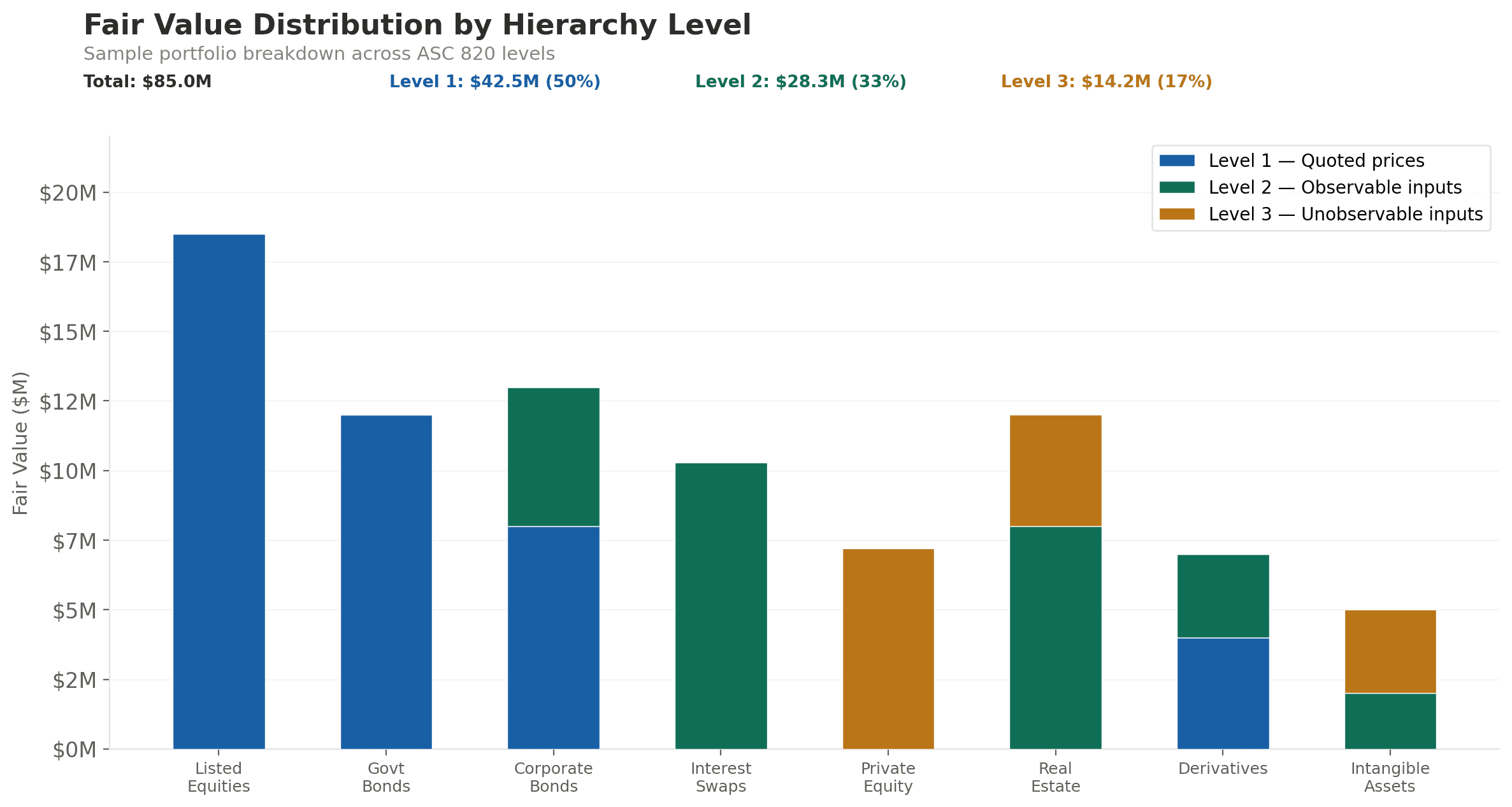

The Fair Value Hierarchy

ASC 820 introduces a three-level hierarchy based on the reliability of inputs used in valuation. This hierarchy helps classify fair value measurements based on the quality and availability of market data.

Level 1 — Quoted Prices in Active Markets

Based on quoted prices in active markets. Most reliable and transparent.

Level 2 — Observable Market Data

Based on observable market data. Includes similar assets or market-based inputs.

Level 3 — Unobservable Inputs

Based on unobservable inputs. Relies on assumptions and estimates. Common in private company valuations.

| Level | Input Type | Reliability | Example |

|---|---|---|---|

| Level 1 | Quoted prices in active markets | Highest | Listed shares |

| Level 2 | Observable market data | Moderate | Government/corporate bonds |

| Level 3 | Unobservable inputs | Lowest (most judgment) | Private equity, intangibles |

The hierarchy moves from the most transparent and market-driven inputs (Level 1) to the most assumption-based inputs (Level 3), with Level 3 requiring the most judgment and documentation.

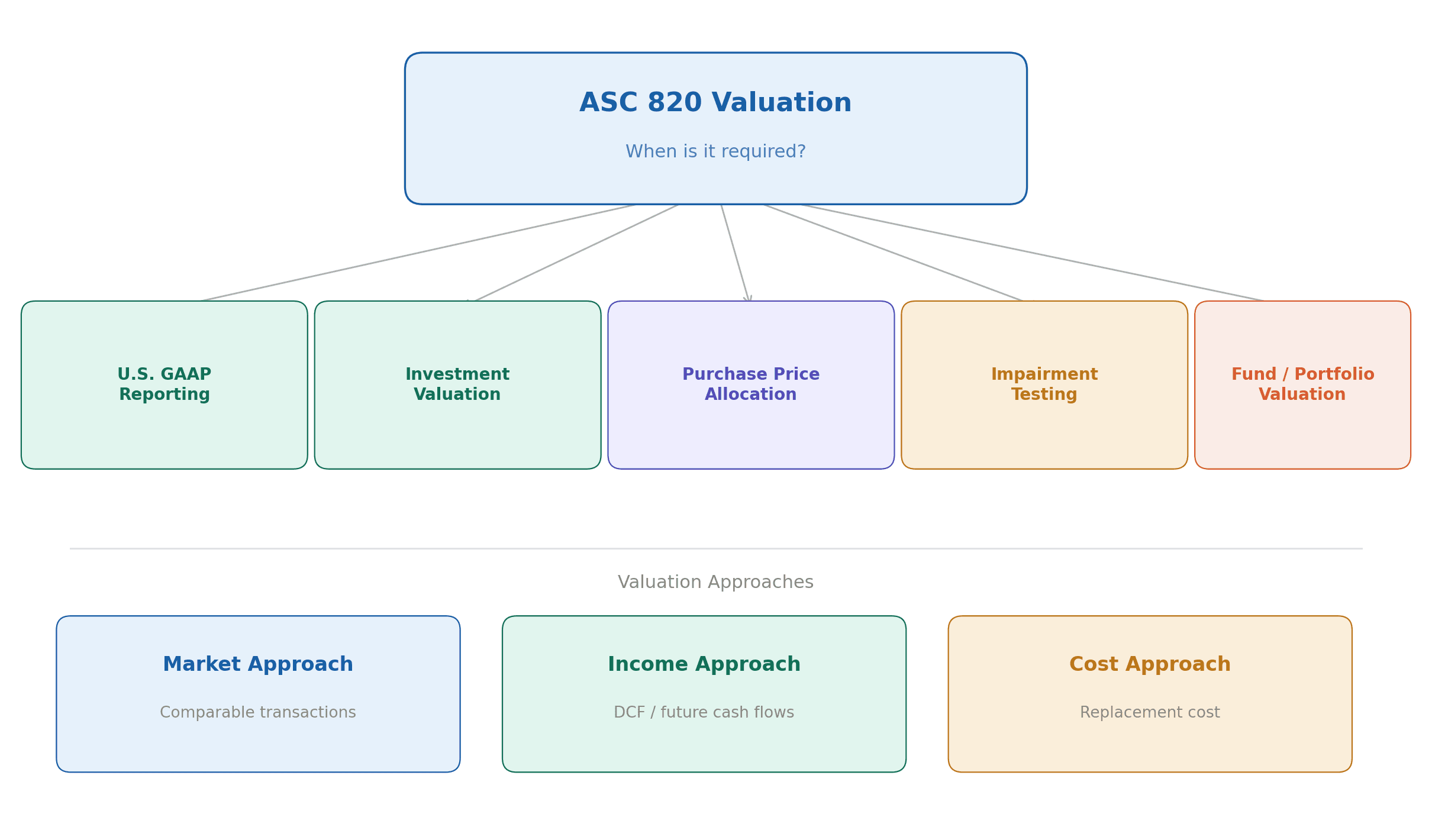

When is ASC 820 Valuation Required?

Companies typically require ASC 820 valuation in several key situations:

- Financial reporting under U.S. GAAP

- Valuation of investments and financial instruments

- Purchase Price Allocation (PPA)

- Impairment testing

- Fund and portfolio valuation

Any company that holds assets or liabilities measured at fair value under U.S. GAAP will need to follow the ASC 820 framework for proper reporting and compliance.

Valuation Approaches Used

Professionals use different valuation approaches depending on the nature of the asset being measured:

| Approach | Description |

|---|---|

| Market Approach | Based on comparable market transactions |

| Income Approach | Based on future cash flows using the Discounted Cash Flow (DCF) method |

| Cost Approach | Based on replacement cost of the asset |

The choice of approach depends on the type of asset, availability of market data, and the level within the fair value hierarchy.

Importance of ASC 820 Valuation

ASC 820 valuation plays a critical role in corporate financial reporting and governance:

- Ensures accurate financial reporting

- Builds trust with investors and stakeholders

- Helps in regulatory compliance

- Supports better financial decision-making

Challenges in ASC 820

While ASC 820 provides a structured framework, companies often face challenges in implementation:

- Lack of market data for certain assets

- Complexity in Level 3 valuations requiring significant judgment

- Frequent changes in market conditions affecting fair value

- Audit and compliance requirements demanding thorough documentation

These challenges make it important for companies to adopt structured tools and platforms that can handle the complexity of fair value measurement while maintaining audit-readiness.

Conclusion

ASC 820 valuation is essential for companies that need to report fair value in a structured and compliant manner. It ensures transparency, improves investor confidence, and supports reliable financial reporting.

For businesses dealing with complex assets or investments, having a proper ASC 820 valuation process in place is not just important — it is necessary. A modern valuation platform can simplify the process by automating calculations, supporting multiple valuation approaches, and generating audit-ready reports aligned with ASC 820 requirements.

Frequently Asked Questions

What is ASC 820 and why does it matter?expand_more

ASC 820 (Accounting Standards Codification 820) is a U.S. GAAP standard that defines how companies should measure the fair value of their assets and liabilities. It ensures valuations are accurate, consistent, and transparent — helping companies maintain compliance and credibility with investors and regulators.

What are the three levels of the ASC 820 fair value hierarchy?expand_more

Level 1 uses quoted prices in active markets (e.g., listed shares) and is the most reliable. Level 2 uses observable market data such as similar assets or market-based inputs (e.g., government bonds). Level 3 relies on unobservable inputs and assumptions, common in private company valuations (e.g., private equity, intangible assets).

When is ASC 820 valuation required?expand_more

ASC 820 valuation is required for financial reporting under U.S. GAAP, valuation of investments and financial instruments, purchase price allocation (PPA), impairment testing, and fund or portfolio valuation. Any company holding assets or liabilities measured at fair value must follow this framework.

What valuation approaches does ASC 820 support?expand_more

ASC 820 supports three approaches: the Market Approach (based on comparable transactions), the Income Approach (based on future cash flows using DCF), and the Cost Approach (based on replacement cost). The choice depends on the asset type, data availability, and hierarchy level.